Sizzling off the approval of its gene remedy for a pair of rare hereditary blood disorders, Vertex Pharmaceuticals (NASDAQ: VRTX) will soon possess one other remedy up for approval, and the financial implications are massive. But they’re no longer massive correct because it stands to crank out billions in extra revenue. As a substitute, the plan is to shell out the equivalent of $100 million so that the functionality novel drug can compete for the market fragment of one amongst its already commercialized medicines as soon as most likely.

What’s occurring here? It be time to dig in and resolve it out so that investors may maybe maybe make a resolution what to enact.

Is that this real news if fact be told substandard news for shareholders?

Per the outcomes of a section 3 medical trial reported Feb. 5, Vertex’s most up-to-date candidate for treating cystic fibrosis (CF), a rare and extreme genetic illness of the lung, is each protected and effective. The remedy is at the moment called “vanza triple” because it combines the molecule vanzacaftor and two other remedy. One amongst the three compounds, tezacaftor, is already in a single amongst the firm’s medicines on the market, though the others don’t appear to be.

In the medical trial, the vanza triple combo carried out no lower than apart from Trikafta, the biopharma’s handiest-promoting product for CF. By one metric — how noteworthy the remedy reduced the level of detectable chloride in sufferers’ sweat — the combo changed into superior, and its aspect bag burden similar. That poses a charming area.

In 2023, Trikafta changed into accountable for roughly $9 billion in gross sales from a high line of roughly $10 billion. If the novel remedy will get approval from regulators at the Meals and Drug Administration (FDA), which management plans to petition for by mid-2024, Vertex may maybe maybe possess two merchandise in mutter competitors with each other on the market simultaneously. There may maybe be seemingly no longer any opportunity for sufferers to take each therapies straight away, and it is a ways unclear whether or no longer there is a probability that a tidy team of sufferers will acknowledge better to the older combination than the novel one.

Therefore, the probability of the vanza triple combination cannibalizing Trikafta’s market fragment is amazingly high. Traders may maybe maybe balk at any resolution to proceed and streak for the approval as they’d moderately continue milking revenue from gross sales of Trikafta for years and years, transitioning to a brand novel product handiest when generic competitors commence to encroach.

And in addition they may maybe maybe balk even more challenging at the management-endorsed belief of expending an asset worth within the ballpark of $100 million to commence the cannibalization direction of even faster. The asset in ask is what’s called a precedence review voucher (PRV), which is a govt-issued fragment of paper that entitles the bearer to bag (you guessed it) a privileged regulatory put within the review levels of the drug approval direction of, thereby reducing the time it takes to streak from submitting the paperwork to getting a resolution on commercialization by a handful of months. In most up-to-date times, many biopharmas possess traded PRVs to each other, preferring to bag cash in desire to set up time, and $100 million is the worth of an identical outdated sale.

Traders are inclined to shock why management appears to be in this kind of chase to torpedo the firm’s most a success product.

One serious detail explains every part

Vertex is no longer being impatient, neither is the resolution to make enlighten of the PRV a unhappy one. Really, the lope changed into carefully calculated and have to seemingly flip out for the handiest for sufferers and shareholders alike. Right here’s why.

Per management, a smaller proportion of revenue from gross sales of the vanza triple drug can be siphoned off to pay out royalties to external parties than with its existing portfolio of CF medicines. So, by commercializing the vanza combination, the enterprise will fatten its revenue margin, despite the fact that it would no longer dramatically expand its revenue, because this can pay fewer royalties.

The usage of the PRV thus implies that management sees the earnings revenue of getting the drug to market moderately faster as being bigger than the sale designate of the voucher. That standpoint is the total extra credible when taking the royalty area into fable, as it greatly changes the commercial revenue of each month the remedy spends on the market.

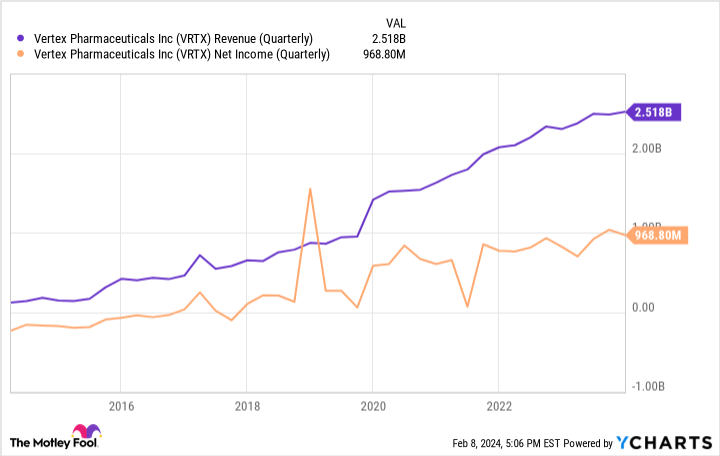

Furthermore, or no longer it is a must-want to have a look at that that is no longer Vertex’s first rodeo by manner of gracefully replacing one amongst its older merchandise with a shinier more recent version that works moderately better. If something else, the firm is an authority at cannibalizing its CF market fragment over and over whereas quiet growing, having commercialized four varied but overlapping remedy in succession over the years. Appropriate look at this chart:

As that that you just can search, the outdated shakeups of its CF merchandise did no longer recede shareholders within the poorhouse, and this time obtained’t either. If something else, here is a bullish setup for the stock. Regardless of every part, it will soon be raking in even extra cash by serving the same core market, and sufferers will bag better remedy, too.

Where to make investments $1,000 real now

When our analyst team has a stock tip, it will pay to listen. Regardless of every part, the e-newsletter they’ve chase for 2 a protracted time, Motley Fool Stock Consultant, has extra than tripled the market.*

They correct printed what they imagine are the 10 handiest stocks for investors to buy real now… and Vertex Pharmaceuticals made the list — but there are 9 other stocks that that you just can be overlooking.

*Stock Consultant returns as of February 12, 2024

Alex Carchidi has no plight in any of the stocks mentioned. The Motley Fool has positions in and recommends Vertex Pharmaceuticals. The Motley Fool has a disclosure protection.

Vertex Pharmaceuticals Will Snarl $100 Million to Tank Its Believe Market Share. Right here’s Why That is a Super Transfer. changed into initially printed by The Motley Fool