Robin Wigglesworth, the author of the guide Trillions, wrote a prolonged but great post about the 2018 to 2020 wintry weather in quantitative fund investing.

A quant wintry weather’s chronicle.

This text is non-paywall.

I would hear to who can repeat this funding stuff in an even bigger map than I might well perchance in on the present time and age. Here is why I worship this article. Lots of the stuff is no longer new to me.

Robin also received on the Rational Reminder podcast to repeat the pondering in the aid of this article:

But I believed I will correct repeat down the significant substances from this article, so as that I build no longer must re-read again and for straight forward future reference.

Historic past of Return Drivers

- 300 years in the past – Sephardi provider provider Joseph de la Vega wrote about a “new” phenomenon of navigating the financial markets in 17th-century Amsterdam:

- Have persistence.

- Accept both earnings and losses with equanimity.

- Benjamin Graham’s Rate Investing

- Charles Dow’s Dow Conception -> Spawn up-to-the-minute technical prognosis of chart patterns.

- 1952 – Harry Markowitz – Notice quant ways to portfolio administration.

- The market itself supplied the optimal balance between risk and return when considered in combination.

- 1960s – Computer programs permit more sophisticated and serious mathematical and knowledge learn into what in actual fact would work. Some conclusions:

- Markets are moderately laborious to beat.

- It would even be so pricey to investigate cross-test to beat the market and it’ll fair no longer be charge it.

- Eugene Fama – Atmosphere friendly Market Hypothesis:

- Hundreds upon thousands of investors always attempting to outsmart one any other intended that the stock market used to be “efficient”.

- We will win a map to beget to which capability that truth correct sit on our fingers and aquire your complete market.

- Section of the motive that spawn off the index funds in the early Seventies.

- 1977 – Sanjoy Basu – Companies with Low stock prices relative to their earnings consistently did better than Fama’s efficient-market speculation will counsel.

- Stephen Ross and Barr Rosenberg – Arbitrage Pricing Conception and Bionic Betas

- Returns of any financial security are driven by a large number of factors on top of the market-risk element.

- 1981 – Rolf Banz

- Outperformance for smaller listed companies

- 1992 – Eugene Fama & Kenneth French – Three-element Mannequin

- Rate and Dimension were mosey factors from the market-risk element.

- 1993 – Narasimhan Jegadeesh and Sheridan Titman – Market Momentum

- Shopping for shares that were already bouncing and selling these that were sliding – might well perchance salvage market beating returns.

- 1996 – Richard Sloan

- Excessive-quality earnings outperformed.

- 2006 – Ang, Robert Hodrick, Yuhang Xing and Xiaoyan Zhang

- Less volatile shares as a neighborhood in actual fact outperform choppier ones.

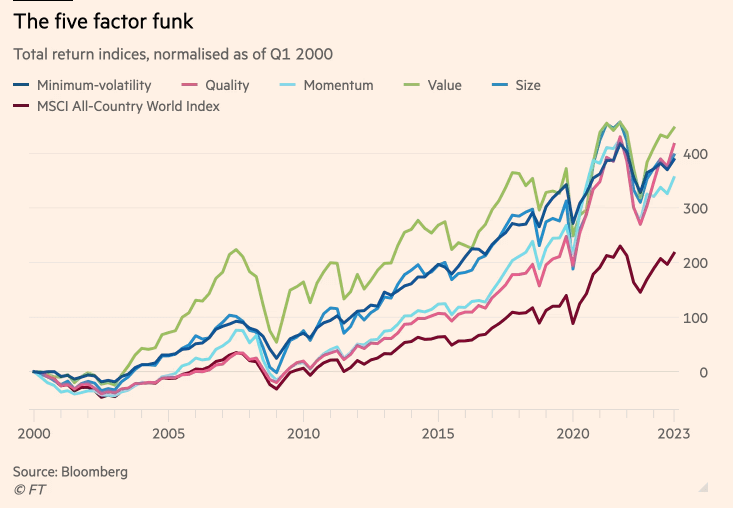

How Nicely the Factors Have Performed – When Knowledge Mined

This chart illustration displays what now we beget always identified:

The outcomes are no longer to gentle if we delivery in the 2000.

In 2000 to 2010 a bunch of the element indexes (market risk + the actual person factors) beget performed better than capitalization-weighted.

The Valuable Foundation Why Factors Must Exist

Folks that align with the foundation that markets are efficient beget that factors are compensation for some invent of risk we’re taking.

We might well fair no longer know what are the risks, but they exists.

Rate shares, to illustrate, are frequently existing in beaten-up, unpopular and shunned sectors, akin to boring industrial companies in the course of tech bubbles. While they’ll underperform for long stretches, at closing their underlying charge shines thru, and they reward investors that kept the faith.

Minute shares build smartly largely because itsy-bitsy companies are likely to fail than bigger companies.

Then there are these that argue that factors exist because as human beings, now we beget our irrational human biases.

As an example, correct worship how we aquire dear lottery tickets for the infinitesimal probability of colossal wins, investors are inclined to overpay for instant-growing, glamorous shares and unfairly shun duller, steadier ones. Smaller shares supposedly build smartly because we’re illogically drawn to names all of us know.

The momentum element, on the different hand, works in conception because investors initially underreact to news but overreact in the end, or frequently sell winners too lickety-split and dangle on to immoral bets for a long way longer than is advisable.

AQR’s Asness studied below Professor Eugene Fama, who is synonymous with the Atmosphere friendly Markets Hypothesis, leans closer to the behavioural camp.

He acknowledged that the market has change into LESS efficient in space of more efficient:

I doubtlessly beget markets are more efficient than the life like particular person does — long-term efficient — but I beget they’re doubtlessly less efficient than I believed 25 years in the past. And so that they’ve doubtlessly gotten less efficient over my profession.

The arena assumes that thanks to things worship the come by that the ubiquity and immediacy of all knowledge has to originate things more efficient. But that’s never been the laborious section.

The same of us who beget the ubiquity and immediacy of recordsdata must mean that prices are more correct are the identical of us who twenty years in the past understanding that social media would originate us worship one any other more.

Cliff Asness

What Basically Differentiates the Quant Funds – Implementation

“These form of are correct semantic labels. They’re in actual fact no longer that thoroughly different,” says Asness. “I beget most quants are deciding on amongst a bunch of factors that we broadly agree on, and then we’ll fight worship cats about the ideal technique to enforce it.”

Cliff Asness

Asness also dispute that premiums reach about because retaining on to those investments are correct unhappy…

To return to the first level, the premiums exist because you would perchance well perchance be taking on some risks, which you would perchance well perchance’t repeat.

He cites what Newfound Compare’s Corey Hoffstein dispute in No Anguish, No Top price:

If it weren’t veritably excruciating, it might probably well perchance doubtlessly salvage arbitraged away. Any strategy that’s rational, done in a plenty of map and that has historically done smartly and never causes you any agonize doubtlessly has a bunch of of us sprint in and originate it trek away.

Cliff Asness

The Case In opposition to Dispute Investing

Some cited that funding methods can no longer work with no discontinuance in sight into perpetuity. Market regimes reach and trek.

When anomalies change into smartly-identified, they might frequently depart.

Inigo Fraser-Jenkins, head of quant methods at Bernstein, wrote a chronicle here about the pain:

Quant funds had been present process one thing of an existential disaster . . . At their core, quant funds strive to apply backtests to future funding choices. But what does it mean to construct quant learn and sprint backtests if the foundations beget changed? There might be a matter to quant past a recent patch of unhappy returns.

If Covid doesn’t count as a regime alternate I don’t know what does. The personality of the protection response is a favorable ruin from the past and directionally factors to the risk of bigger inflation but with out a commensurate enlarge in staunch charges. Here is no longer like recent a protracted time, with profound implications for factors and asset allocation.

Inigo’s article has about a correct nuggets.

He beget’s authorities or political insurance policies that prevent pure recessions beget impeded reversion to the mean, and that is a colossal pain:

Others beget identified that element investing might well fair be lecturers and their overzealous knowledge mining. The asset administration enterprise is generally on the stumble on out to stumble on what’s going to even be packaged up and sell for giant administration charges.

Clif Asness has written a paper that offers a counterpoint to the foundation that the most standard funding factors can no longer be replicated.

There isn’t a favorable motive in the aid of what resulted in Quant Iciness, but…

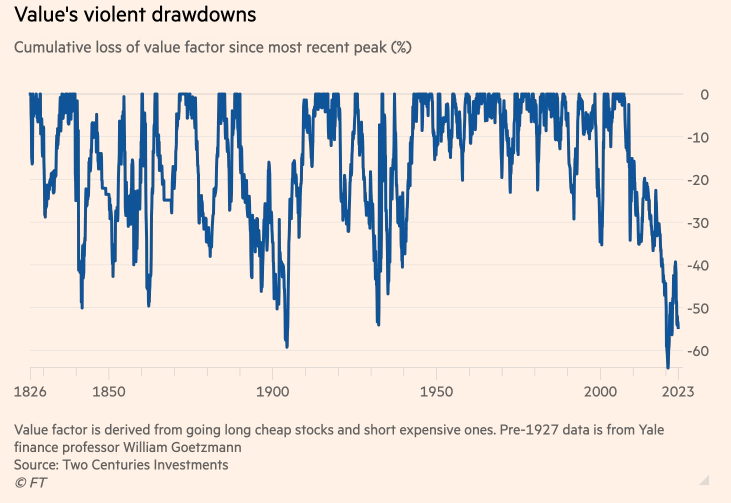

Asness’ conclusion is that tag did very badly.

Rate had one among the more severe drawdowns in 200 years:

This chart above will even be stumbled on on Two Centuries investments, and they in actual fact beget a momentum drawdown one. It displays that such loss in efficiency to declare is no longer out of the standard. Rate top price doesn’t always existing up.

Two Centuries, in their most modern post build beget an the explanation why factors decay:

Kyith is the Owner and Sole Creator in the aid of Investment Moats. Readers tune in to Investment Moats to learn and affect stronger, less assailable wealth foundations, easy the technique to beget a Passive funding strategy, know more about investing in REITs and the nuts and bolts of Energetic Investing.

Readers also divulge Kyith to learn to devise smartly for Monetary Safety and Monetary Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Within the intervening time, he works as a Senior Solutions Specialist in Insurance Starting up up-up Havend. All opinions on Investment Moats are his rep and would no longer listing the views of Providend.

You might well conception Kyith’s current portfolio here, which makes employ of his Free Google Stock Portfolio Tracker.

His funding broker of assorted is Interactive Brokers, which permits him to put money into securities from thoroughly different exchanges all the map thru the arena, at very low price charges, without custodian charges, conclude to set currency charges.

You might well read more about Kyith here.

Latest posts by Kyith (look all)